As condominium buildings across Canada continue to age, major repair and replacement projects have become an increasingly pressing reality for condo boards and property managers. Whether it’s a leaking roof, aging elevators, or a deteriorating underground parking, these projects eventually become unavoidable and they carry significant price tags.

As condominium buildings across Canada continue to age, major repair and replacement projects have become an increasingly pressing reality for condo boards and property managers. Whether it’s a leaking roof, aging elevators, or a deteriorating underground parking, these projects eventually become unavoidable and they carry significant price tags.

The challenge many condo corporations face today isn’t just navigating the project specifications, it’s understanding how these projects could be paid for and what options are available to them. Understanding the different funding options that are available, and the trade-offs involved with each one, can be very beneficial to boards, managers, and owners alike.

The Reserve Fund Study and Critical Assumptions

A reserve fund study is intended to help condominium corporations plan for major repair and replacement projects over the long term. It estimates when common element components will need to be repaired or replaced, what those projects may cost, and how much the corporation should contribute to the reserve fund annually based on these estimates.

However, reserve fund studies depend heavily on assumptions. One of the most critical assumptions is the assumed annual inflation rate. Typically, reserve fund studies use CPI-based inflation of around 2-3% per year. In a stable construction market, this is likely a reasonable baseline. But recent years have shown that construction costs can rise much faster than CPI would suggest.

When the actual cost of construction rises materially above the assumptions used in the reserve fund study, a corporation can find itself underfunded even if it has closely followed the study’s recommended funding plan. The board may have acted responsibly, but the market just moved faster than anticipated.

The result may be a reserve fund shortfall. We can define this as a situation where a condo corporation does not have enough available reserve funds to complete a necessary project in the near-term, while also maintaining the financial capacity to address other future repair and replacement obligations.

Construction Inflation and Why Shortfalls Are So Common Right Now

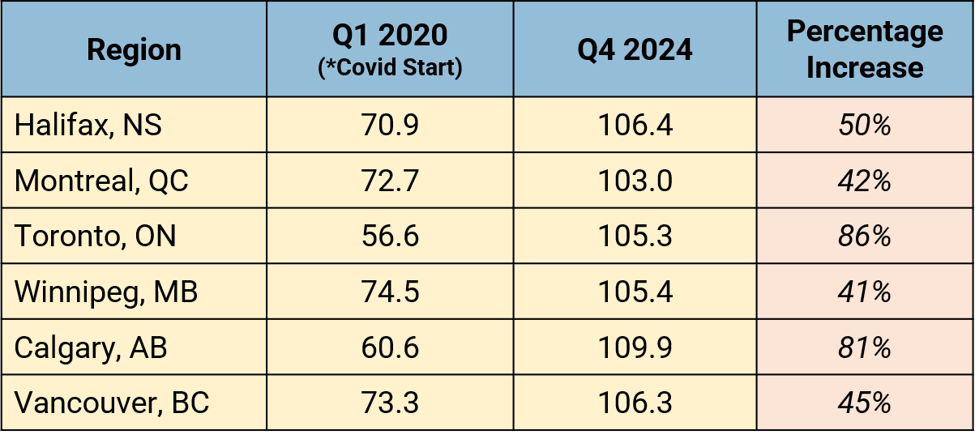

Source: Statistics Canada, Residential Building Construction Price Index.

Statistics Canada reported that construction inflation for residential buildings in the Greater Toronto Area rose approximately 86% from the start of 2020 to the end of 2024. This sharp increase was largely due to the COVID-19 pandemic and the associated supply-chain disruptions.

In contrast, assuming a typical CPI-based rate of 3% per year, that would have resulted in a cost-increase of only 16% over that same timeframe. This would mean that a corporation following those recommendations has underestimated construction inflation by about 70% over those five years (according to the estimates from Statistics Canada).

This gap between projected and actual costs has resulted in reserve fund shortfalls across the country. Boards that once felt financially prepared are now confronting a very different reality, particularly those who have renewed their reserve fund study at some point in the past few years and are now seeing updated project cost estimates for the first time since.

The Three Available Funding Options

When a reserve fund shortfall is identified, condo boards generally have three funding options available to them. Each comes with distinct implications for the corporation and for individual unit owners.

-

Deferring the Project

Delaying repairs could allow the reserve fund to save more reserve fund contributions over time before the work begins. The key issue is that the project cost will likely continue to rise with each year that passes, as demonstrated in the content above. Per the estimates from Statistics Canada, a $1-million project in 2020 may have risen to $1.86-million by the end of 2024. Beyond the financial impact, deferred maintenance could also accelerate deterioration, reduce property values, and create safety risks.

-

Special Assessments

A special assessment levies a one-time financial responsibility (either in one lump sum or multiple installments) on each unit owner to cover the funding gap. While this approach is direct and doesn’t carry interest costs, it can be financially disruptive for residents. In some cases, special assessments can exceed tens of thousands of dollars per unit, creating a significant financial burden for owners.

-

Condo Corporation Loans

An increasingly popular solution is a loan to the condo corporation. Rather than deferring projects or levying sudden special assessments on owners, a condo corporation could borrow the necessary funds needed to complete the project works and spread the costs involved over a longer period. The loan payments can be structured within the common fees, provided on an optional basis, or combined with special assessments to reduce the financial burden. The flip side is that the loan will come with additional interest costs for the corporation.

Making an Informed Decision

Reserve fund shortfalls are a practical challenge and not necessarily a reflection of poor governance. The key takeaway though is that there are options available to boards faced in such situations, and there are parties that are able to support them through that process.

It never hurts to explore your options and do your due diligence on the different funding options available. Most lenders who specialize in condo corporation financing will meet with boards at no cost to discuss how a loan to the condo corporation may compare to deferral or special assessments. That discussion can help boards make more informed decisions on behalf of their community.